Dollar Cost Averaging vs. Lump-Sum Investing

When it comes to investing, two principles consistently guide long-term success: diversification and staying invested. While these ideas sound simple, they can be difficult to execute, especially when markets are near all-time highs or experiencing heightened volatility. This raises common questions among investors:

Is there an optimal way to invest? dollar cost averaging or lump-sum investing?

While mathematics can offer insights, the best strategy is ultimately the one an investor can follow with confidence and discipline.

Is Dollar Cost Averaging Right for You?

Markets go up and down. Whether it’s a presidential election, geopolitical developments, inflation trends, or interest rate decisions, investors are constantly exposed to news that can influence short-term market sentiment. It’s also important to remember, just because the market is at a peak, it does not mean it is “due” for a decline.

Ironically, many investors find it psychologically difficult to invest in both rising and falling markets, fearing they may be buying at the top during rallies or that prices will continue to drop during downturns. This emotional tension often leads to hesitation, bad timing, or remaining on the sidelines altogether.

Dollar cost averaging (DCA) helps address this challenge by replacing emotional decision-making with structure and consistency.

How to Invest After a Liquidity Event

Determining when and how to invest becomes even more complex after a liquidity event, such as, significant annual bonus, the sale of a business, an inheritance or legal settlement.

While investing efficiently is critical for long-term wealth creation, short-term volatility can discourage even the most disciplined investors. This is where dollar cost averaging can play a valuable role.

With a DCA approach, investors commit to investing a set dollar amount on a predetermined schedule. This reduces the temptation to react to daily market movements and removes the pressure of finding the “perfect” entry point.

Which Method Performs Best Over Time?

From a purely mathematical standpoint, lump-sum investing often has a performance advantage over very long time periods, because capital is fully exposed to the market sooner. However, investing is not that simple. Human behaviour, emotions, and risk tolerance play equally important roles.

Dollar cost averaging may not always be the optimal mathematical strategy, but it often proves to be the most behaviourally sustainable strategy, especially for those starting wealth creation. Most importantly, being invested sooner, rather than waiting for perfect timing, remains one of the strongest predictors of long-term success.

For many investors, dollar cost averaging already happens automatically through employer-sponsored retirement plans. Each pay cheque contribution is, by definition, a form of systematic investing. The precise frequency matters far less than having a consistent, automated plan in place. However, many in the middle east have no form of company pension, so the responsibility is on us.

In contrast, lump-sum investing involves committing all available capital at once. While this can lead to higher returns in strong markets, short-term performance becomes heavily dependent on how markets behave immediately after the investment.

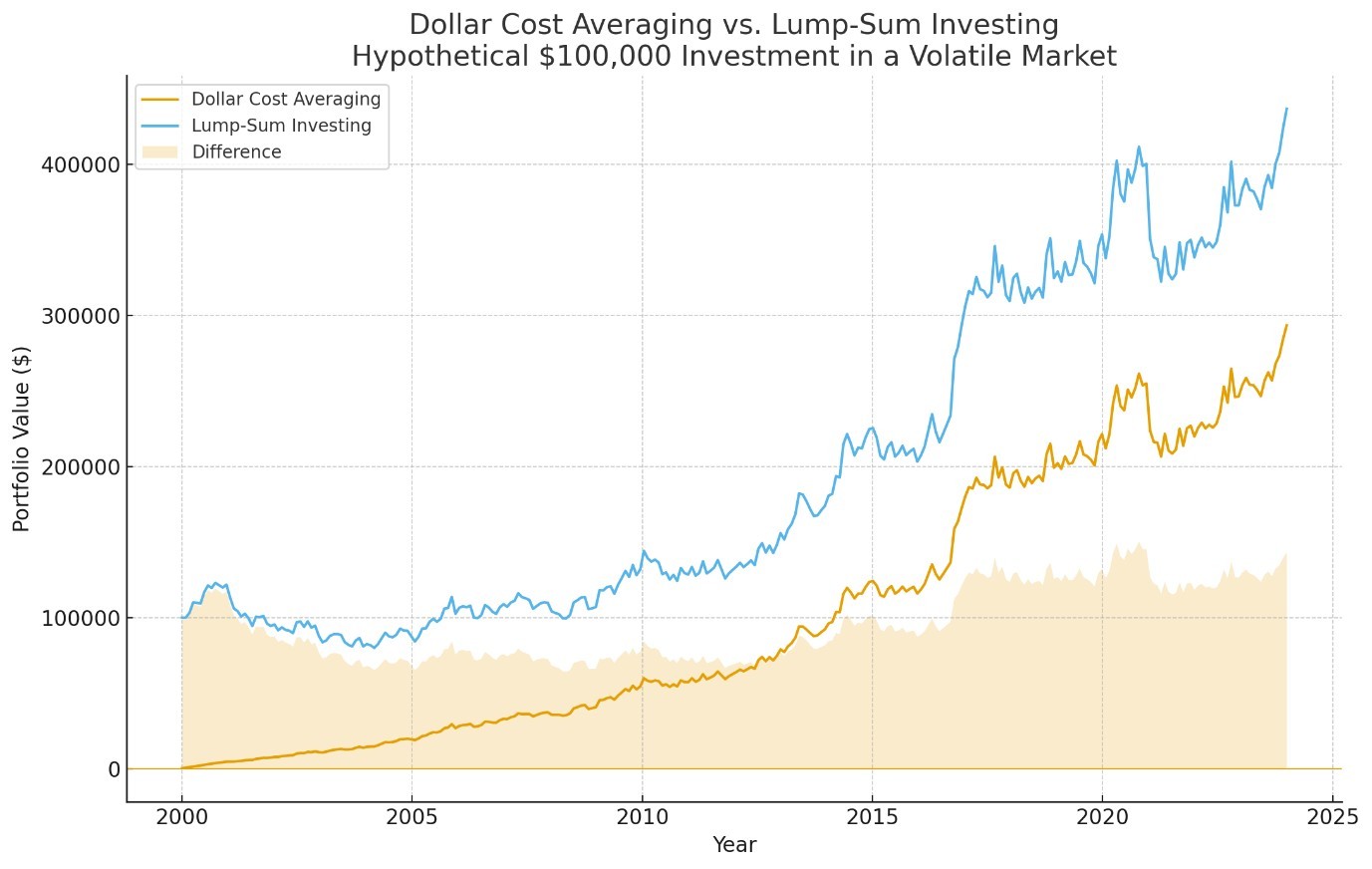

Historical Perspective: Lump Sum vs. Dollar Cost Averaging

A useful example begins in the year 2000, when equity markets were at elevated valuations before the dot-com crash.

An investor who deployed $100,000 into the S&P 500 at that time experienced immediate losses, followed by a recovery, and then another sharp decline during the 2008 financial crisis. The market eventually recovered and went on to benefit from the prolonged bull market that followed.

By contrast, a hypothetical investor who invested that same $100,000 gradually over time using a dollar cost averaging strategy experienced less extreme entry point risk, accumulated shares at more favourable prices during downturns, and achieved improved risk adjusted outcomes along the way.

Choose What Feels Comfortable.

Dollar cost averaging enhances portfolio stability, while lump-sum investing often produces higher absolute returns over time, but with greater volatility on large amounts of money, which can be daunting.

DCA May Help Reduce Emotional Investment Decisions.

One of the biggest benefits of dollar cost averaging is its impact on investor behaviour. By committing to a predetermined investment schedule, investors are less likely to; react to market headlines, delay investing due to short term fear, overcommit during periods of market euphoria.

Final Takeaway

Please consult with your financial advisor and/or tax professional to determine the suitability of these strategies. All views, expressions, and opinions in this communication are subject to change. This communication is not an offer or solicitation to buy, hold, or sell any financial instrument or investment advisory services.